We have been living in our tiny house full-time since mid-May 2012 – a year and a half now. Sometimes the house feels WAY TOO SMALL and my busy brain starts wondering (again), “WHY are we living like this???” Why don’t we just get a loan?

One reason we chose to build our own tiny house was to escape the debt of a MORTGAGE, the typical requirement of home “ownership.” (I use quotes because we often say that we own our homes, but if we’re paying a mortgage, the bank is actually the owner.) Read all of our reasons for going Tiny on our Why Tiny? page.

During one recent period of tiny house discontent I started thinking about interest rates – only 5%!!!! Well jeez, that is low… 5% of $200,000… is only …. $10,000! That’s nothing! We find a $250,000 house, put $50k down… borrow $200,000 + $10,000 interest… Why are we so against mortgages??

(Personal note: I have never had a mortgage, always rented, primarily due to a deep loathing of debt, and secondarily due to the fact that I never could have gotten the funds needed to buy a condo in L.A. or Denver, especially not after the crash of 2008 – in 2009 I applied for a mortgage loan and was approved for $80k. You can’t buy jack for $80k in Denver. Shane, on the other hand, has had mortgages since he built his first house at the age of 18. He was always able to build / buy low and sell high, until the 2008 crash, when home values dropped about $100k in his town. The mortgage company would not reconsider the value of his home, continuing to charge him mortgage payments on a home worth $280k when he could only hope to sell it for $180k. His mortgage payment was also about $300 a month higher than what he could rent the house for.)

Shane found an online mortgage calculator to show me the actual cost of a 5% loan… Seeing the amount of money paid on top of the listing price instantly rekindled my interest in living in a Tiny House!

So, while 5% of $200,000 is indeed $10,000…. that is not AT ALL how mortgages are calculated. (I realize this is elementary to many, but I love seeing the numbers – makes me feel better about living in 200 sf.)

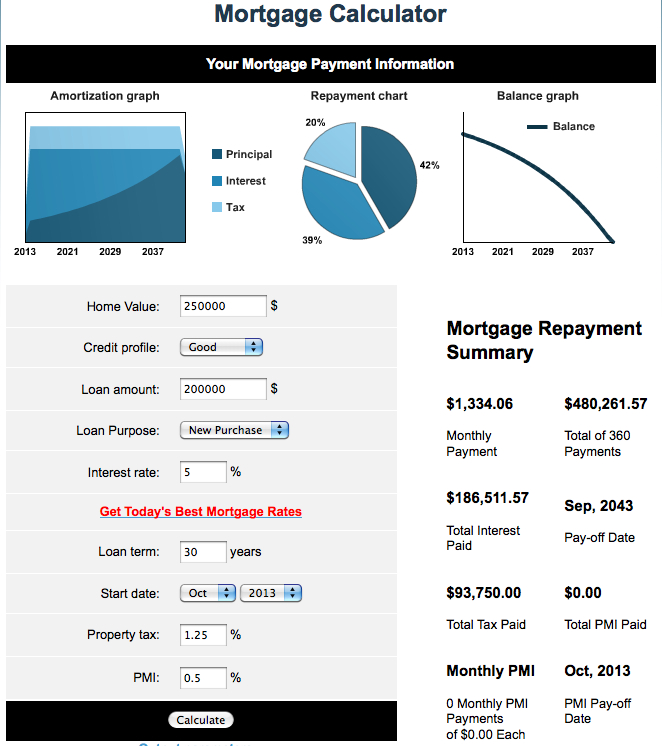

We would actually end up paying the bank $186,511 (over 30 years) in order to borrow that $200,000. Which is 93%, not 5%. (You don’t hear anyone raving about record time low interest rates of 93%!)

And that house that was listed at $250,000? We would end up paying $480,261! Wow.

An image from an online mortgage calculator:

And if the $93,750 total tax is on top of the $480,261… that’s $574,011! Over half a million dollars for a 2 BR / 2 BA starter home…

Now the story we’re told here in America is that Home Ownership is the American Dream, you aren’t anything unless you own your own home. I seriously think the bankers might be behind this bit of American folklore – it definitely seems in their best interests (pun…) to get people to “own” their own homes.

Well, the reason so many intelligent and logical people do choose to pay banks is because they feel that they are “throwing their money away” on rent, and a mortgage is… Equity, right? An investment in your future…

Eq-ui-ty : noun : fairness or justice in the way people are treated [incredibly ironic?]

: finance : the value of a piece of property (such as a house) after any debts that remain to be paid for it (such as the amount of a mortgage) have been subtracted

So let’s take a look at Equity:

$250,000 house

$50,000 down payment

= $200,000 loan / mortgage = $1,334 per month + $3,125 taxes per year

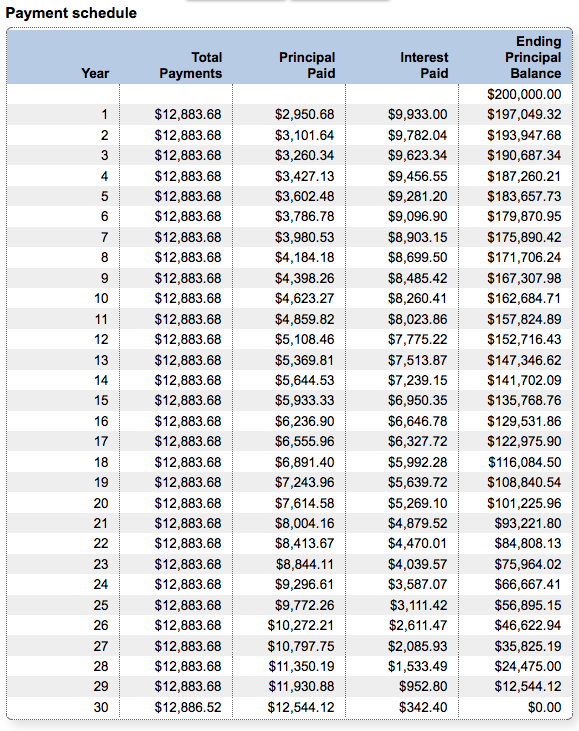

After 5 years I still owe $183,349. Gulp. But… my house is now worth $280k instead of the $250k I paid for it. So, I sell, maybe to make a profit, maybe because I have to move, who cares why, everybody’s doing it.

$280,000 – $183,349 = $96,651 “profit”

– minus the $19,264 closing costs (5.1% to the realtors, 1.78% tax) = $77,387 “profit”

– minus the $15,625 in taxes I forked out over 5 years = $61,762 “profit”

= barely enough to make a down payment on a similarly valued home and start paying rent to the bank again.

Oh, and what about the $50,000 I so generously donated to the bank?

– minus the $50,000 down payment = $11,762 “profit”

AND what about the $1,000 per year I had to put into fixing the HVAC system, installing gutters, removing that tree, etc. etc.

= $6,762 profit.

I paid 5 years of monthly payments at $1,334 = $80,040 to live for 5 years, and I’ve only saved up / profited $6,762 when I sell.

The other way to own a home, the way that we’re trying to do it (and many other tiny housers / thrifty dwellers), is to live small, save, and build a house debt-free.

Over five years of living in the tiny house we will pay $934 LESS per month ($1,334 – $400) = $56,040 + that $50,000 down payment = $106,040 saved up / profited over 5 years.

Tiny house too tiny? What if you rent a smallish place for $900 per month – over 5 years you’ll be able to save $26,040 from not paying a mortgage + that $50,000 down payment = $76,040. WAY more than the $6,762 profit from buying and selling.

So why exactly is home ownership so wonderful? Because the banks make money on our borrowing. Granted, if you stay in your home for 10 years or 20 years, you can actually come out ahead, though not really enough to retire on…

According to Bankrate calculators you’d still owe $101,225 after 20 years of paying on a $200,000 loan. That’s more than half of the loan! After two DECADES of paying it off.

I think people just get comfortable with the cost of housing being $1,000 – $2,000 a month and just pay it. For their entire lives. But how is that not Serfdom? And banks have some incredible leverage because it takes SO long to save up $200,000 (legally…ha) to buy a house outright. So for us, the Tiny House may be INSANELY small but it is allowing us to save up enough money to get into a more comfortable house without paying interest to a bank.

This was a LOT of numbers, if you’ve made it this far, thanks for sticking with me!

I’m curious about other people’s tactics to own a home debt free…

[ I’m sure there are errors in my math / logic / understanding of the mortgage system – forgive me. I know I’ve omitted things like utilities, paying a mortgage off early, homeowners insurance, mortgage insurance, etc.]